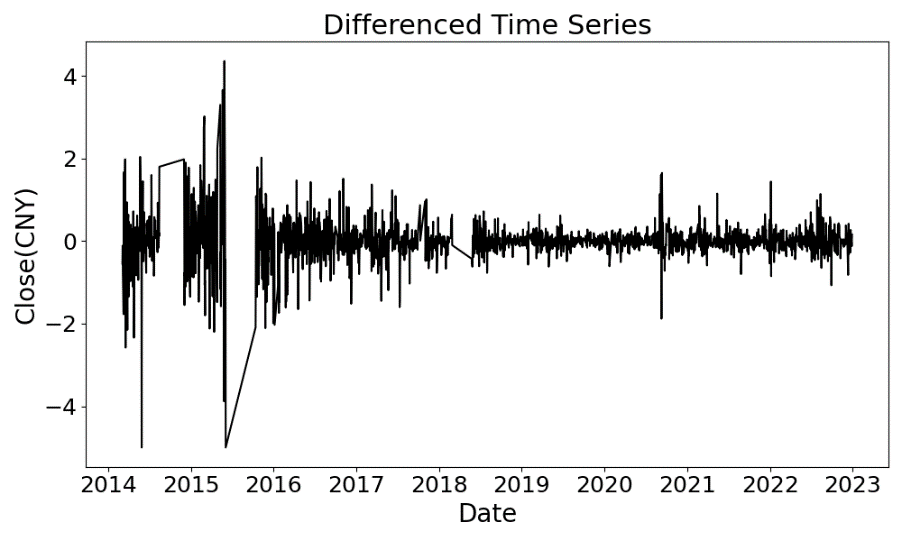

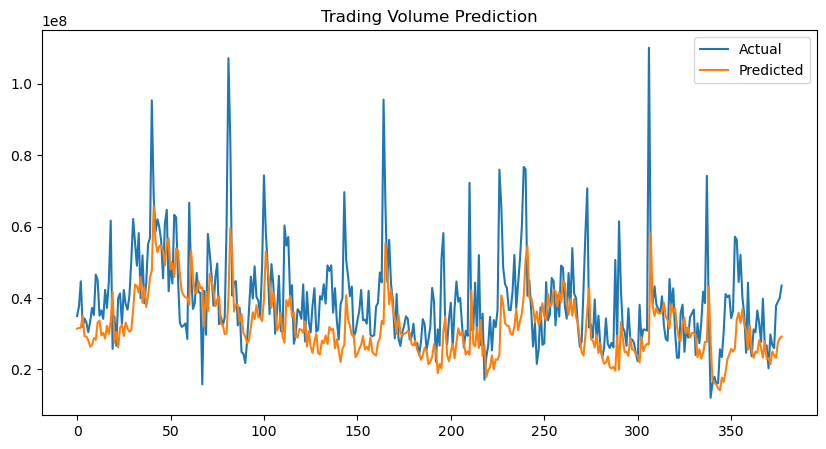

Time series analysis plays a pivotal role in diverse domains, facilitating critical tasks such as forecasting, classification, and anomaly detection. This paper introduces a multi-task learning (MTL) model utilizing a deep learning framework to simultaneously predict three key financial indicators: trading volume, closing price, and volatility. By leveraging shared representations across tasks, the MTL model captures intricate dependencies and enhances generalization, outperforming single-task benchmark models—ARIMA and univariate Deep Learning (DL). The MTL model achieves over 50% reduction in MAE and RMSE compared to ARIMA and approximately 10% improvement over DL. The results demonstrate the ability of MTL to exploit inter-task relationships, delivering more accurate and robust forecasting for stock markets. This work highlights the potential of multi-task learning framework in enhancing financial time series forecasting.